On Thursday, July 3rd, the U.S. House of Representatives passed the One Big Beautiful Bill Act (OBBB). Is it "big"? Yes. You can read all 870 pages of it here if you’d like: [OBBB]. Is it "beautiful"? That's for you to decide.

Below, I’ve summarized the key provisions that I believe are most relevant to our clients.

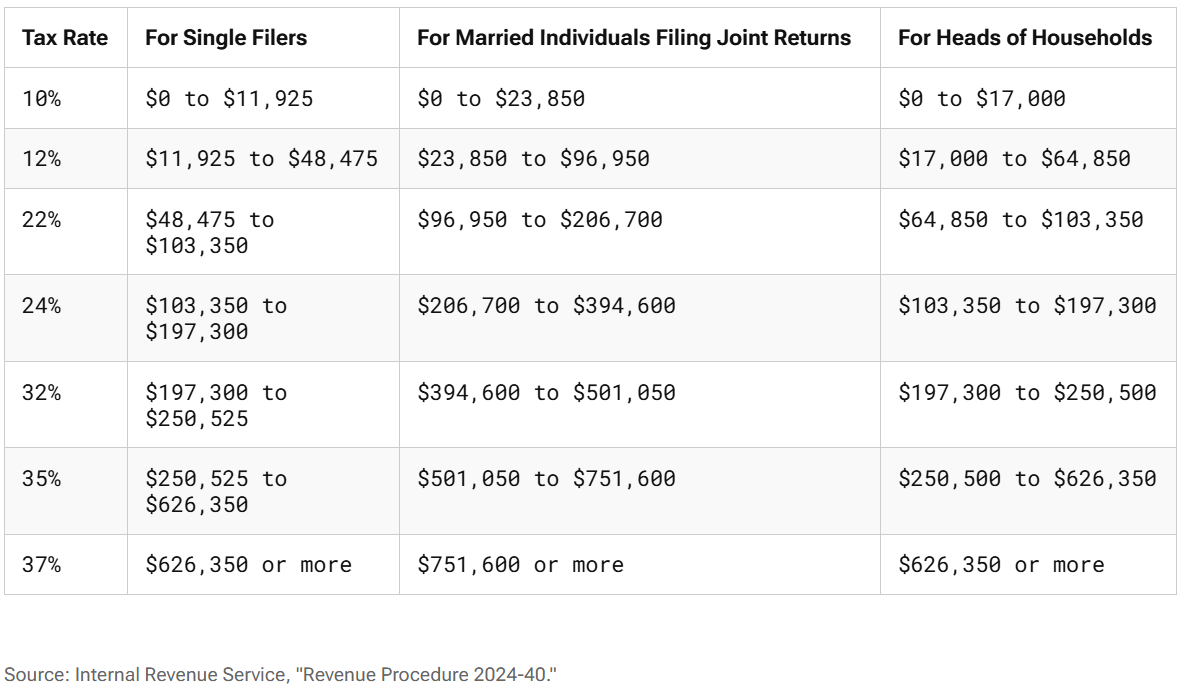

The 7 ordinary income tax brackets (10%, 12%, 22%, 24%, 33%, 35%, and 37%) are now permanent. "Permanent" means they do not expire on a set date. They can certainly be changed with future legislation.

For reference, here are the taxable income breakpoints for the marginal brackets in 2025:

This is pretty much a continuation of current law, as no action by Congress in 2025 would have lead to these tax rates reverting back to the pre 2018 tax law.

The 2018 tax law limited the itemized deduction for state and local taxes (AKA the SALT Cap) at $10,000. The OBBB increases that amount to $40,000, however there is a phaseout as adjusted gross income exceeds $500,000 (this phaseout starts at $500k both for single filers and married filing joint). Once your adjusted gross income is $600,000 or more, the SALT deduction is once again capped at $10k for you as it was before the passing of the OBBB.

That means if your income goes from $500k to $600k, your taxable income could potentially increase $130,000 despite only making $100,000 more, due to losing $30k of the SALT deduction from the phase out.

This part of the Bill is effective starting in 2025, and is only effective through 2029.

A new deduction of up to $25,000 is available for qualified tip income, phasing out at $300,000 AGI for joint filers ($150,000 for single).

Joint filers can now deduct up to $25,000 of overtime income, and single filers up to $12,500.

Starting in 2026, taxpayers can deduct:

…in charitable donations without itemizing. This mirrors the temporary deduction allowed during the COVID-19 pandemic.

You can now deduct up to $10,000 annually in auto loan interest without itemizing.

Starting in 2025 we have the updated standard deductions listed below:

New: Senior Bonus Deduction

An additional $6,000 deduction is available for seniors over age 65 ($12,000 for a couple). Phases out at $150,000 AGI (joint) or $75,000 (single).

Effectively, a senior couple under the phaseout limit could have a standard deduction of $46,700, shielding much of their Social Security income from taxation.

Beginning in 2026, the federal estate and lifetime gift tax exemption increases to $15 million per person, indexed for inflation. That’s up from the current $13.99 million.

This new account type resembles a blend between a Roth IRA and a 529:

The maximum child tax credit has increased from $2,000 to $2,200 and the credit is now indexed to inflation.

A new $1,700 nonrefundable tax credit is available for cash or marketable security donations to organizations that provide elementary or high school scholarships.

However, states may opt out. If a state declines to participate, none of its students will be eligible for scholarships funded under this provision.

The expiration of the enhanced advanced premium tax credits for health insurance was not addressed in this Bill, which means without further acts of Congress before yearend we are heading back to the "subsidy cliff" for marketplace health insurance plans. That means once your household income goes over 400% of the federal poverty level you will receive zero health insurance subsidies. For a family of 2 in 2025, that means an income over $84,600.

This could lead to sharp increases in health insurance costs for pre Medicare retirees if not addressed.

I saved the opinion section for the end, because I know most people haven't read this far. The sunset of the 2018 tax law that we all planned for is not going to occur after all. The continuation of current income tax brackets provides some certainty into the future, but we are raising the debt ceiling once again by $5 trillion, which shows that no one in Washington is terribly serious about balancing the budget. The only hope is that we will grow our way out, and that remains to be seen.

Like every omnibus bill there are some real head scratchers in the OBBB, some of which are noted above. I'm sure if you want extensive political insights and opinions you can get your full dosage on that elsewhere. We'll try and stick to financial planning here.

Meredith Wealth Planning, LLC is a registered investment adviser. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. Past performance is not indicative of future results. Investments involve risk and are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed here.

A quick chat to get to know each other and learn more about what you're looking for in an advisor

We know that working with an advisor is a big decision, take some time & sleep on it

When you're ready, we get started with our planning process