Three weeks ago CNBC reporter, Andrew Ross Sorkin, appeared on 60 Minutes to discuss his new book, 1929, and the parallels between that era and today (full clip here: 60 Minutes).

This interview has made waves throughout social media and other publications often being framed as Mr. Sorkin predicting another Great Depression scenario for equity markets, but if you actually watch the full interview and listen to what he says (or doesn't say) it is not that different than the messaging we routinely give clients at Meredith Wealth Planning.

When asked if he expects a crash, Sorkin replied:

"The answer is we will have a crash. I just can't tell you when and I can't tell you how deep, but I can assure you, unfortunately, I wish I wasn't saying this, we will have a crash".

I couldn't agree more, actually I think I have said nearly the exact same thing to clients many times over the years. Market downturns are the rent you pay to live in the stock market neighborhood. They are to be expected and planned for, and any attempt at avoiding them should correspond with the likelihood of lowering your lifetime investment returns.

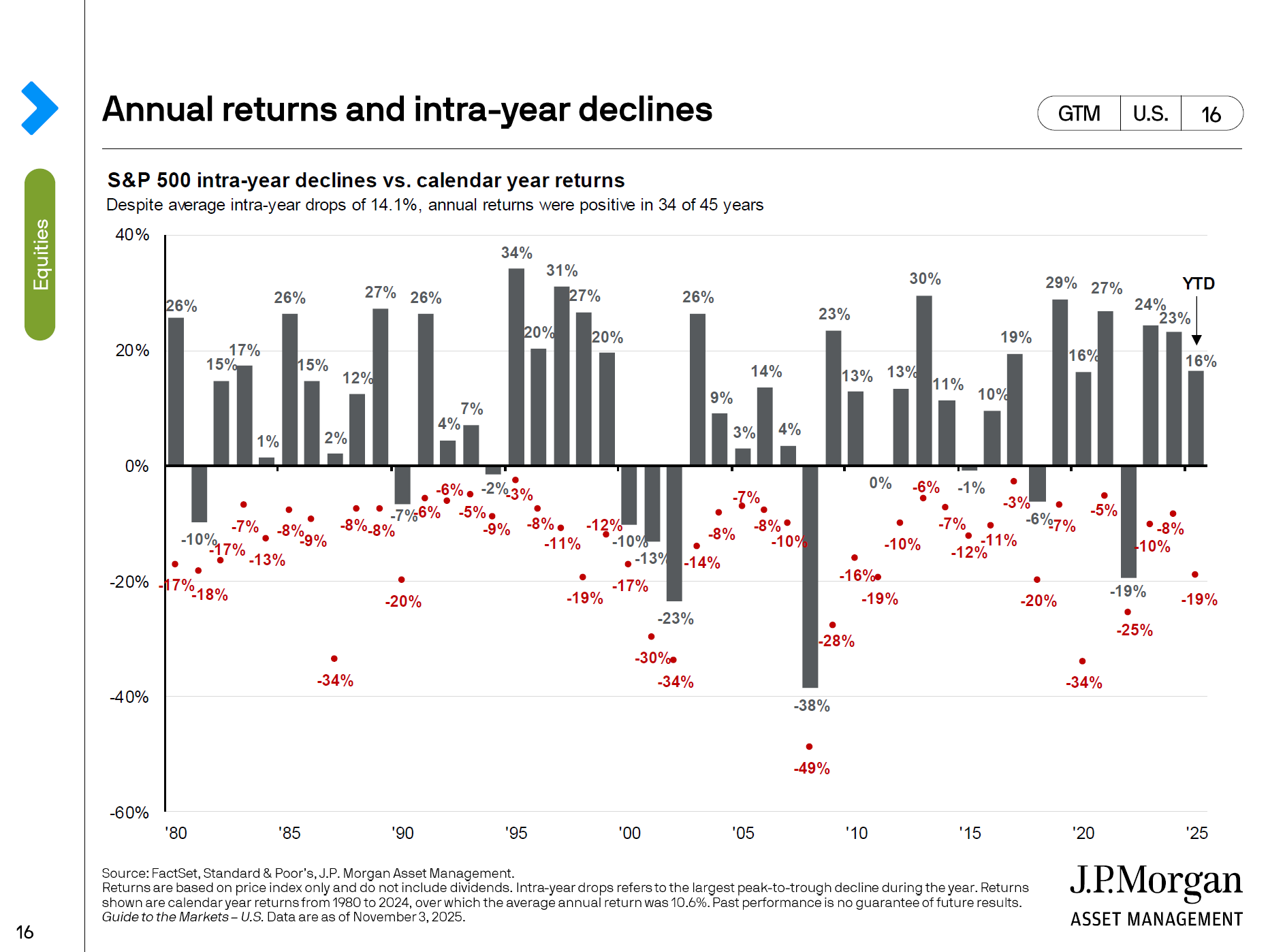

The chart below I have shared numerous times before, where the red dots depict that largest intra year decline in the S&P 500 every year going back to 1980. Despite the average intra year decline of 14.1%, the average annual return from 1980 - 2024 was 10.6% with 34 of the 45 years being positive. If you are planning to try and avoid the next red dot episode, you are likely overconfident in your predictive abilities and overthinking your investment strategy.

"You can't predict, you can prepare". -Howard Marks

Equity markets are not the beach. There is no green flag flown to signal markets are now safe to enter. Risks rarely come from the direction everyone is watching. The real danger is the shark in the water that hasn't been spotted (COVID, 9/11, Black Monday, OPEC embargo etc.).

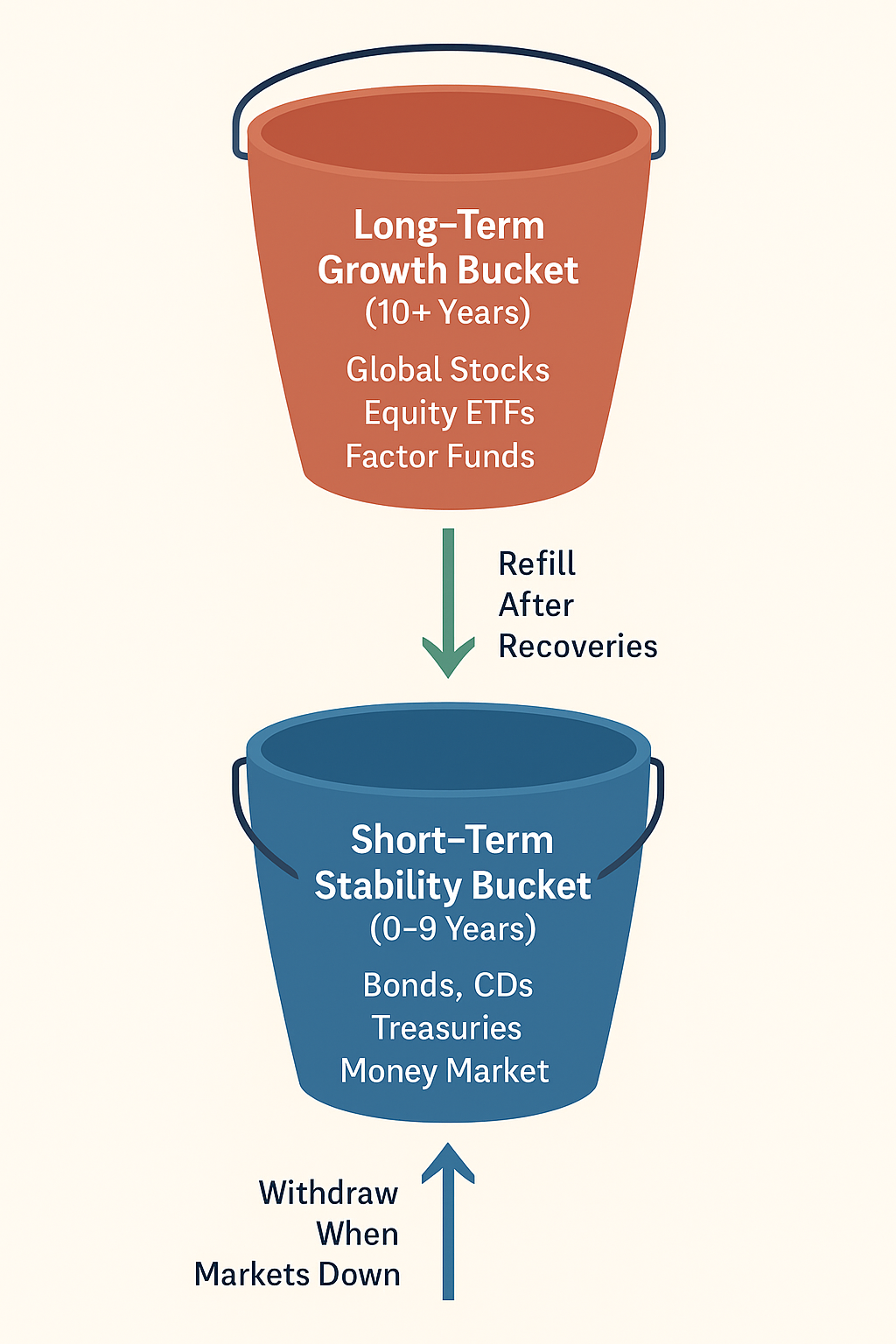

How can you prepare as Howard Marks suggests? My favorite approach is a simplified bucket strategy. Your portfolio can be viewed through the lens of two buckets as described below:

Knowing your short to intermediate cash flow needs are secured, you can sleep soundly through the market's storms. This is how you prepare, not predict.

Mr. Sorkin did bring up an important issue regarding private investments now being pushed onto 401(k) investors, and how Wall Street suggests this a is a good thing for retail investors. 60 Minutes decided to ask the CEO of Blackrock, Larry Fink, who very much supports this movement.

Just as margin loans expanded access to speculation in 1929, today’s push to put private equity into 401(k)s is being marketed as “democratization”, but that word should make investors pause.

In 1929 it was very uncommon for the common man to own stocks so Wall Street started allowing retail investors buy stocks on margin by putting only 10% down for their purchases while borrowing the other 90%. This was marketed as a great concept at the time, as it allowed more participation in equity markets for the retail investors. It did not end well.

Today there are hurdles for the common man to invest in private equity, and Larry Fink suggests this would give retail investors the opportunity to invest in great companies before they actually go public.

I am skeptical of Mr. Fink's arguments. Private equity investing generally comes with higher fees, less transparency, and less liquidity. In June, Benjamin Schiffrin, of Better Markets wrote a post about why private market assets do not belong in 401(k)s. In the article he states:

"So why the push to open up the private markets to 401(k)s? It’s not because workers want more options in their 401(k)s, and certainly not less liquid and hard-to-value assets. And it’s not motivated by plan sponsors, who worry that anything seen as expensive, complex, or risky could lead to lawsuits. Instead, it’s because private equity firms are finding it harder now to raise money. The “private capital industry has struggled to raise new money in recent years from institutional investors such as pensions and endowments.

As a result, private market firms eye America’s vast retirement system. The industry now wants a slice of the $12 trillion pie that comprises America’s retirement accounts."

History doesn’t repeat perfectly, but it often rhymes. Whether it’s margin loans in 1929 or private equity in 401(k)s today, “new access” often benefits the sellers more than the buyers. For most investors, sticking to transparent, low-cost, liquid investments remains the best way to capture market growth without being someone else’s exit liquidity.

Meredith Wealth Planning, LLC is a registered investment advisor. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any securities. Past performance is not indicative of future results. Investments involve risk and are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed here.

A quick chat to get to know each other and learn more about what you're looking for in an advisor

We know that working with an advisor is a big decision, take some time & sleep on it

When you're ready, we get started with our planning process