There are 3 subjects that are taboo to discuss at family dinner: religion, politics, and bond funds. For this blog post, I am going to put religion and politics aside but am certain to ruffle a few feathers as I make the case for owning bond funds over individual bonds.

First let's recap why anyone should even own bonds in the first place.

I would never blindly suggest that anyone reading this should or should not own bonds. That's a conversation to be had with your financial advisor or Chat GPT, preferably whichever one hallucinates less.

Anyone that has owned bonds over the last 5-10 years might be asking themselves why should they own bonds at all. The declines we have had in the equity markets have been short lived, and the bond market has experienced one of its worst periods ever, especially after accounting for inflation.

However if we look at the last 50+ years of data, bonds as an asset class have produced respectable returns for a lower risk investment.

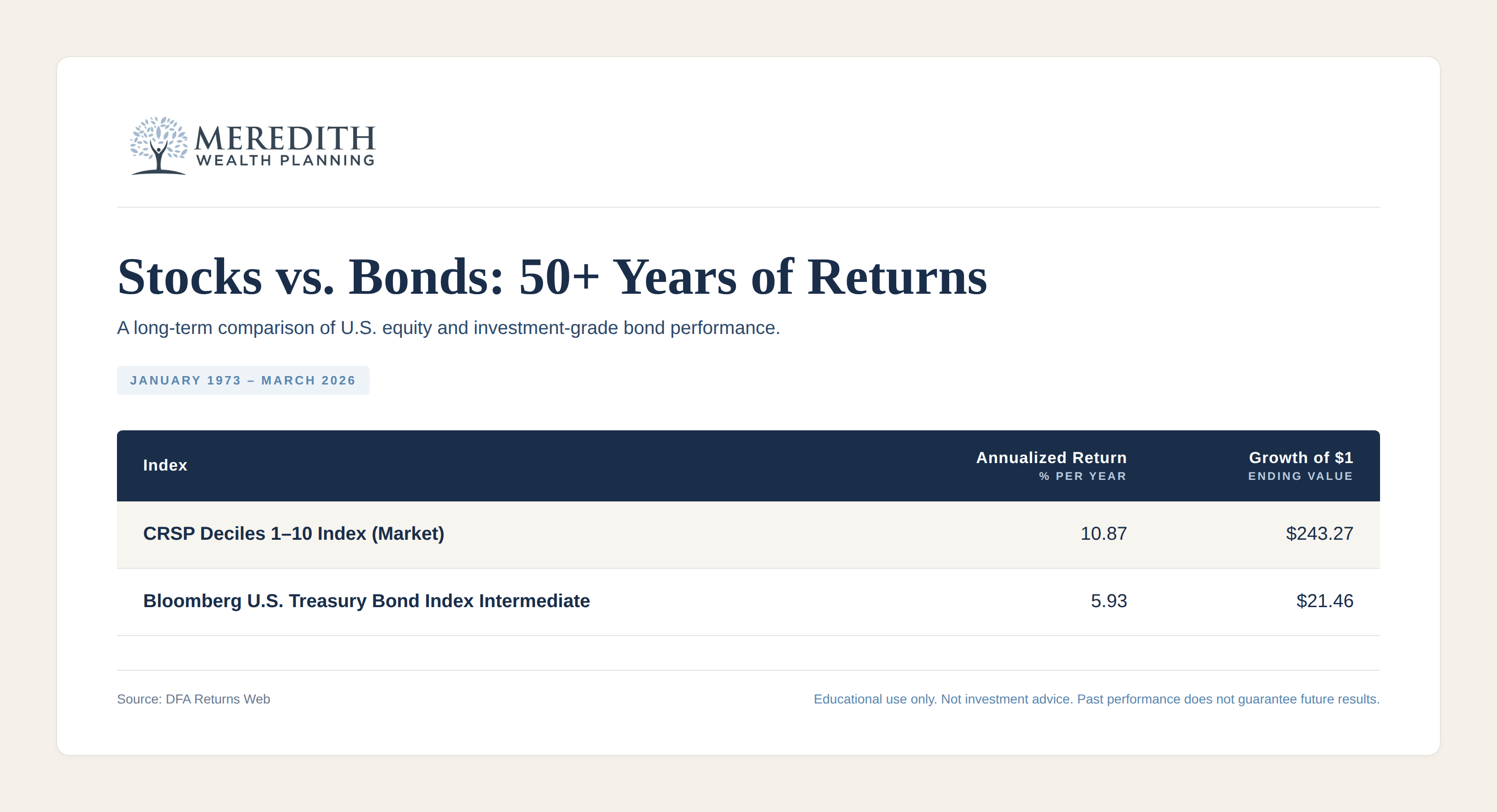

Inflation during the period shown in the image above (01/1973 - 03/2026) was 3.93% annualized, so we saw both stocks and bonds both produce real returns (before tax!) above the inflation rate.

The US equity market is represented by the "CRSP Deciles 1-10 Index". Over the last 50+ years the growth of $1 invested in equities is more than 11x of that invested in bonds. This surprises some people who are not too familiar with the power of compounding interest, as a 10.87% return (equities) is not even twice that of a 5.93% return (bonds), yet it leaves you with more than 11x more dollars after 53+ years.

History shows us that the opportunity costs of owning any bonds instead of all equities can be quite large, so why do it? I have written about this subject before (How Much Should a Retiree Have in Stocks?), but to recap, simply lowering your portfolio's volatility so you feel better in a market downturn is not a great reason to own bonds. Barring a default, a bond has a predetermined outcome and can be helpful for a retiree wanting to safeguard some of their future cash flows.

As we see in the chart below, bonds historically have held up well during periods of equity market stress. Out of the 639 months from 01/1973 - 03/2026, 239 of them produced negative equity market returns. During those months, bonds (as measured by the Bloomberg U.S. Treasury Bond Intermediate Bond Index) averaged a 0.39% monthly gain.

There is an endless debate amongst investors and financial professionals whether one should just go buy bonds directly, or own them through a mutual fund/ETF. Lets review the arguments each side might make.

Now let's attack the arguments for individuals bonds one point at a time.

This is one of the stronger arguments for individual bonds in my opinion, but it is weaker than it appears. The idea is that if you buy say a 3 year Treasury Bond at 4% interest, you know you will collect 4% annually on that bond and the receive the entirety of your principal back in 3 years.

From my experience, most investors do not need a defined outcome on a defined date. When a bond matures, they often mull it over for a bit and renew it into a new bond. Of course a fund would handle that for you automatically.

Today, if someone really needed a defined outcome on a defined date, they could utilize defined maturity bond ETFs which diversifies your money across hundreds of bonds and still has a set maturity date. These are offered through major asset management firms for as low as 0.08% in expenses.

A bond mutual fund or ETF has an expense ratio, which today can be as low as 0.03% a year. One could avoid that expense by buying the bonds directly themselves, and cutting out the intermediary.

Missing is the fact that when retail investors go to buy individual bonds directly, they are often paying far wider bid-ask spreads than what institutional buyers like Vanguard or Blackrock would pay. A fund's expense ratio is frequently offset by the pricing advantage they get on execution.

Also, a bond fund commonly has hundreds of bonds in it so unless you are going to directly buy hundreds of different bonds yourself then you are likely giving up diversification by going with a smaller amount of holdings.

This is pretty similar to the defined outcome on a defined date argument. If an investor knows they will need $100k from their portfolio every year for the next 10 years, then could ladder out a bond portfolio to have that amount maturing each year.

Liability matching is a concept that was developed for pension funds and insurance companies, entities with known contractual obligations on specific future dates. For individual investors, that level of precision is rare in my experience. Tuition payments, home renovations, car purchases, vacation spending, are all variable, flexible, and adjustable in ways that a pension obligation is not.

Even when there are genuine predictable future liabilities that can be matched, to get adequate diversification across corporate bonds an individual investor would still need to buy hundreds of bonds at retail spreads to ensure an accidental concentration in a AAA rated Lehman Brothers bond doesn't wreck their retirement.

The individual bond argument is that you know exactly what is coming in via bond interest payments and on what dates. However, bond fund investors also receive regular income and in most cases more frequently.

Individual bonds often pay interest semi-annually. Most bond ETFs or mutual funds distributed monthly or quarterly.

With individual bonds you have no way to automatically reinvest the interest that is paid, whereas in the fund you can set it up to auto-reinvest and buy more shares, compounding your future interest payments. An individual bond holder may experience some drag to interest payments not being redeployed in a timely manner.

When fundholders panic and redeem shares en masse, the bond fund manager may be forced to sell bonds into a depressed market to meet redemption requests.

Of course, investors do not generally flood out of bond funds in calm markets, they are more likely to flee when interest rates are rising and bond prices are falling (ironic, because that is exactly when their expected bond returns are increasing). Those environments do not spare individual bondholders. Their bond prices are also declining in the same proportion for the same reason.

The individual bondholder's advantage here is the ability to hold until maturity and recover par value. But a bond fund investor can do something similar, simply hold for a period equal to the fund's average duration, at which point rising rates are likely to have worked in their favor, with early price declines more than offset by higher reinvestment rates on distributions

The debate over individual bonds versus bond funds is a debate about control versus efficiency. Individual bonds offer the illusion of control. You know your coupon, you know your maturity date, and you know your principal is returned at that time. Most of that control is either replicable with the right fund or less meaningful in practice than it appears on paper.

Bond funds, and particularly bond ETFs, have won this argument. They offer broader diversification, lower effective costs, and automatic income reinvestment. For investors who want the precision that individual bonds are celebrated for, a specific duration, a specific maturity horizon, the modern ETF landscape makes that entirely achievable. Want short duration? There's a low-cost fund for that. Intermediate? Same. Long? Take your pick. An investor today can build a bond portfolio targeting virtually any duration they want, at a fraction of the cost and complexity of assembling individual bonds, and adjust it with a single trade as their needs evolve.

Individual bonds can still make sense in a narrow set of circumstances.. For everyone else, the case for bond funds is powerful.

Disclaimer: Meredith Wealth Planning, LLC is a registered investment adviser with the SEC. This blog post is for educational and informational purposes only and should not be considered investment advice, a recommendation, or an offer to buy or sell any security. All investing involves risk, including the possible loss of principal. Past performance does not guarantee future results. References to specific securities, funds, or companies are for illustrative purposes only and do not constitute a recommendation. Meredith Wealth Planning and its clients may hold positions in the securities discussed. For more information, please review our Form ADV and Form CRS.

A quick chat to get to know each other and learn more about what you're looking for in an advisor

We know that working with an advisor is a big decision, take some time & sleep on it

When you're ready, we get started with our planning process