Index funds are great products and have served millions of investors well. Despite their great qualities they are our second favorite choice at Meredith Wealth Planning.

This surprises people since our investment philosophy is "evidence-based" and the evidence suggests that low cost index funds, like those offered through Vanguard, are very hard to beat.

Plus, financial legends like Warren Buffett and John Bogle have stated repeatedly over the years that people only need to buy index funds. Let's dive into what makes index funds great, what the flaws are, and what we find to be a better alternative.

Before index funds became popular, many investors relied on actively managed mutual funds to diversify broadly and outsource management of their portfolios to professionals. This sounds great on paper. Ideally a skilled portfolio manager can pick the good companies to invest in while avoiding the bad ones.

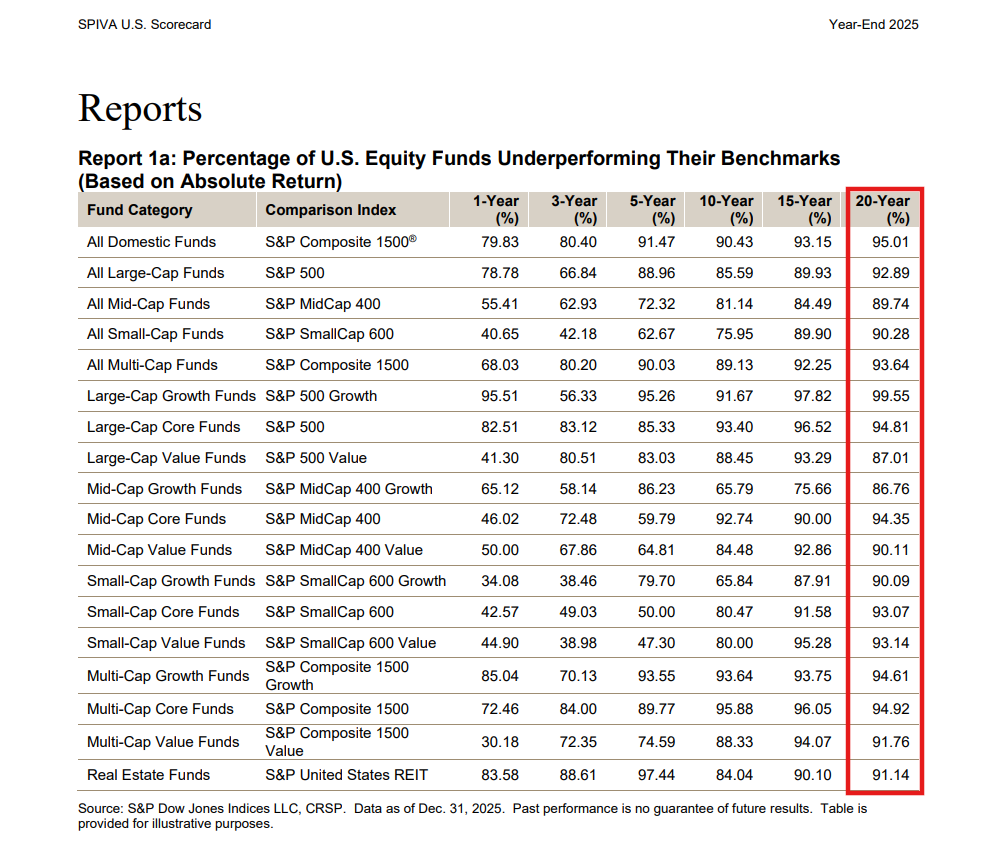

Ultimately though, actively managed funds often underperformed unmanaged indices like the S&P 500. Over the last 20 years, most categories in the US saw over 90% of actively managed mutual funds underperforming their benchmarks.

Any excess returns earned by the actively managed mutual funds were eroded through their higher fees and higher tax implications.

As that evidence became more clear, mutual funds and ETFs were created to track the S&P 500 Index, and many other indices as well. Why would one pay a manager for skill when it was shown they didn't have enough skill to overcome their costs?

The rise of index funds came with great perks to the retail investor such as:

Many large brokerage firms today still live in the Dark Ages, continuing to use higher expense actively managed mutual funds. Why is this? I suspect it is because of money.

If you take a look at the most recent revenue sharing disclosure statement from Edward Jones (here's link for you!), you will notice that in 2025 they received over $325 million from the mutual fund partners (which are predominantly actively managed mutual fund managers). This does not mean the investments are bad, but it does lead one to question the motive behind their recommendations.

While index funds get a lot of things right they also have structural weaknesses that are rarely discussed.

Index funds have become incredibly popular. By some estimates there are 2,000 - 3,000 index funds available in the United States. Today an asset manager can create an index for any bizarre idea they have, then create a fund to track it, and label it as an index fund. Want specifics? Have a laugh:

While I cannot fathom recommending funds like this to clients, apparently there is a market for them.

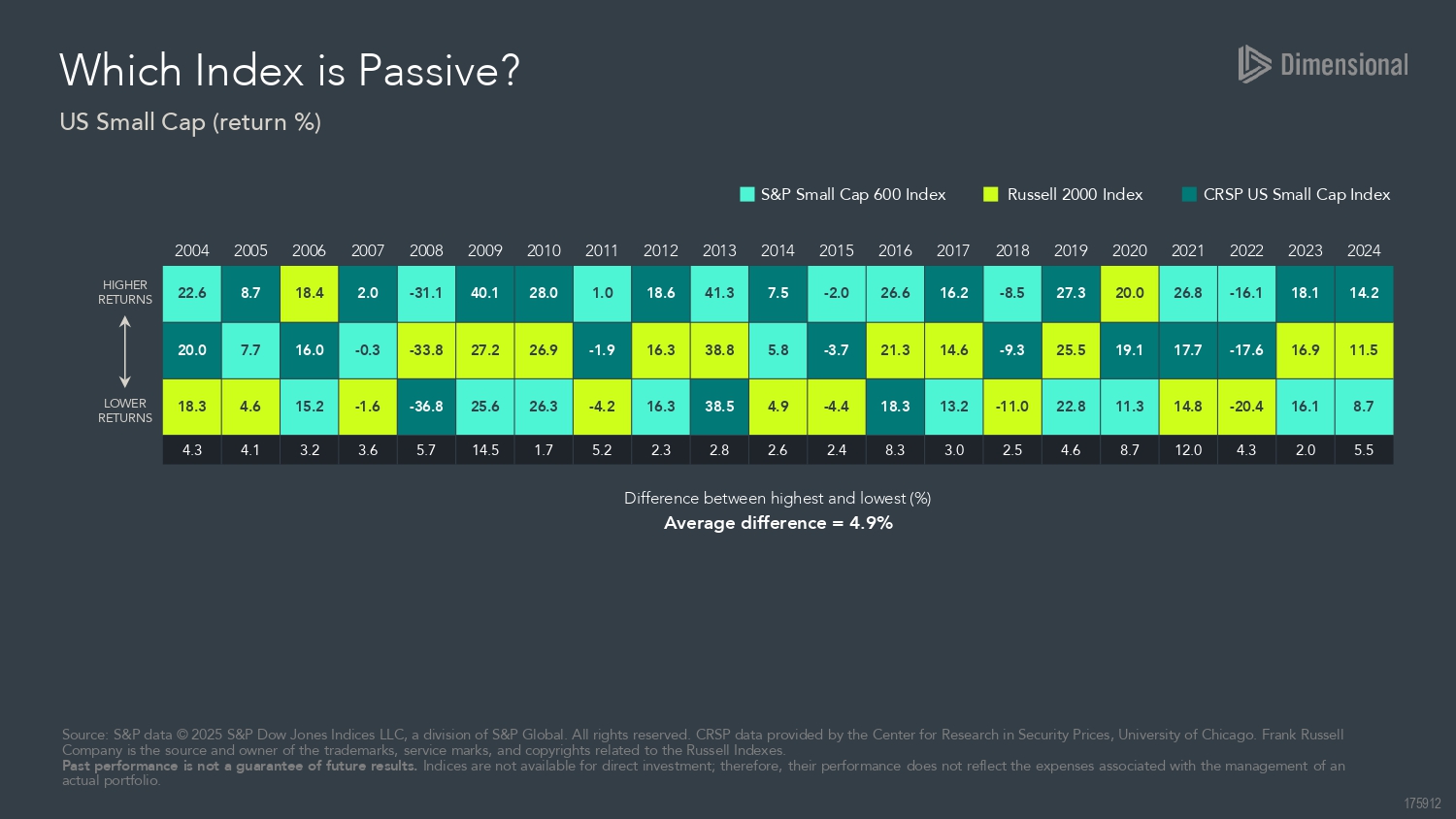

But even in more streamlined investment categories like US Small Caps, we see a bit of a muddy pond. Below we see a comparison of 3 different US Small Cap Indices. Vanguard has an index fund for each of these 3 different indices (the ticker symbols are VIOO, VTWO, and VB). So if you are contemplating which small cap index fund to buy, how will you choose? The return differences can be substantial.

Index fund providers still make active decisions such as which countries to include in their index, how often to reconstitute the index, and when to announce the changes for reconstitution events.

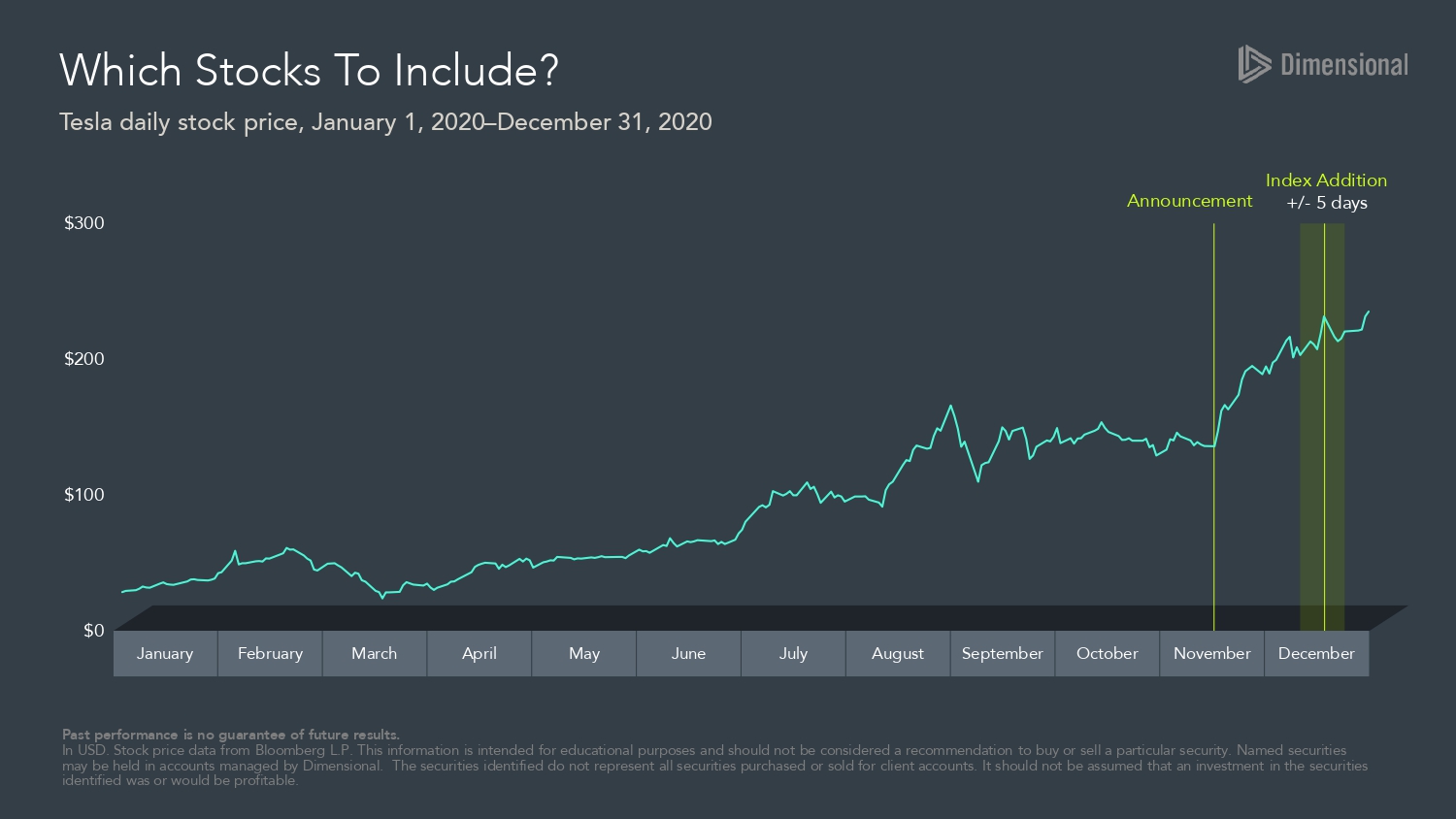

When an index fund announces a new addition to the index (such as the S&P 500 did with Tesla in November of 2020) investors pour in to front-run the trade before it is added. Below we see the announcement of Tesla's inclusion to the 500 Index and the subsequent dramatic increase in the stock price before it was actually added. Holders of the 500 Index missed that appreciation that was front-run by traders:

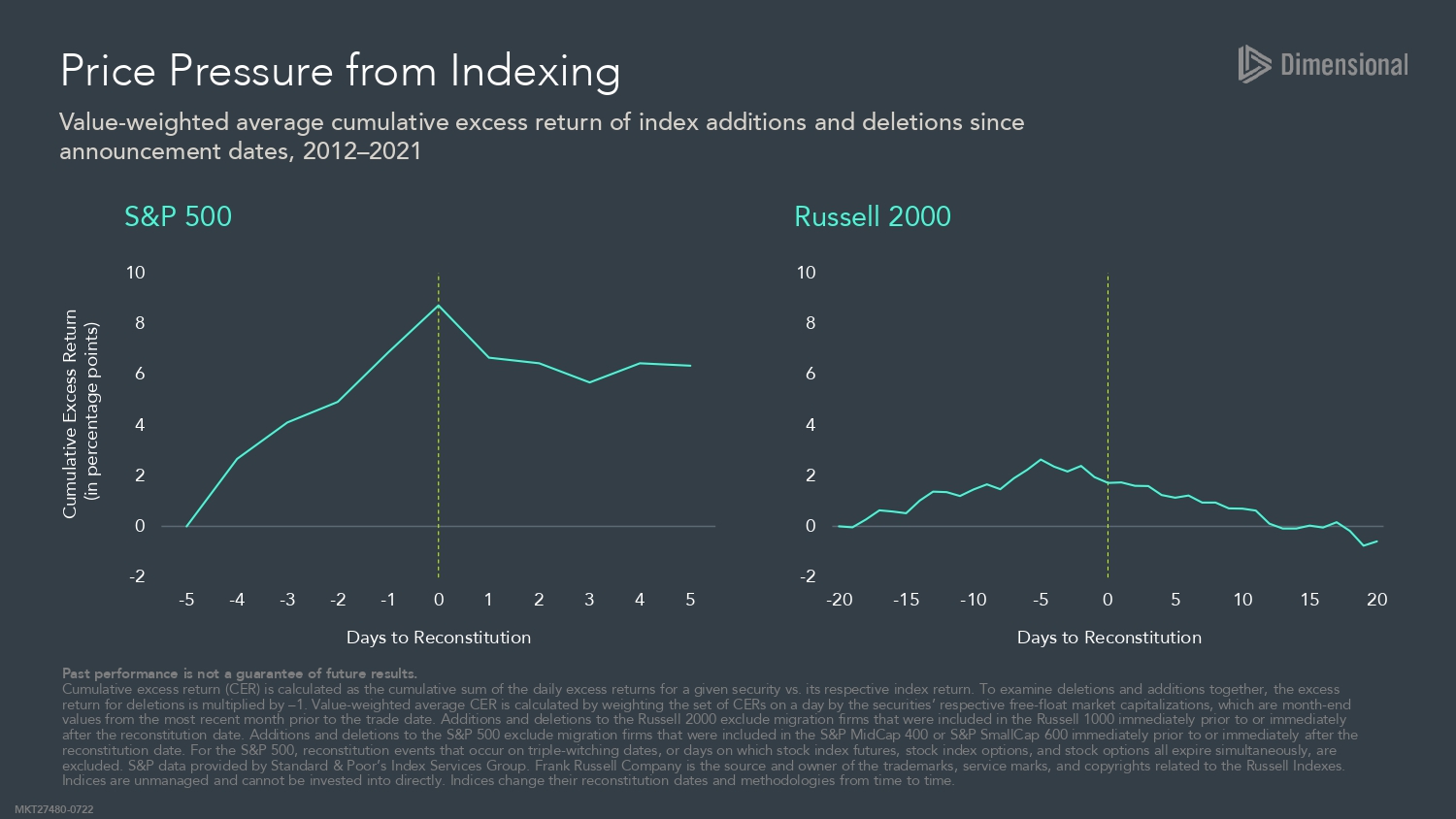

This is not an anomaly. If we look at the data below from 2012 - 2021, what we see is a consistent pattern that stocks run up in value before they are added to the index and taper off thereafter.

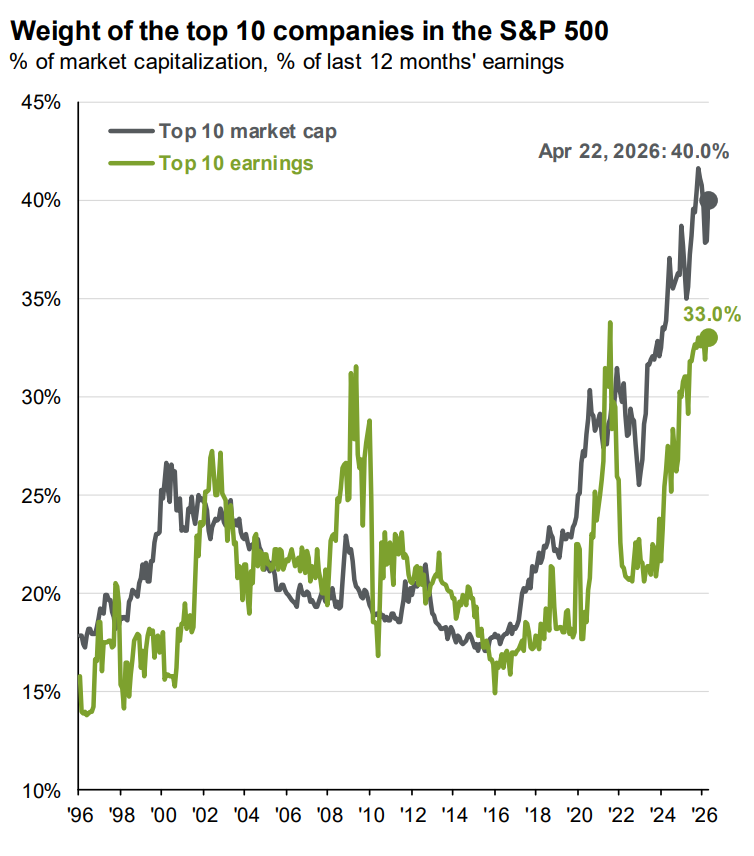

It is generally believed that index funds like the S&P 500 are well diversified across 500 stocks, but today about 40% of the index is invested in just 10 companies. This is much higher than any point in the last 30 years. An investor may be a bit more concentrated that they initially believed.

Index funds like the S&P 500 also pay very little attention to relative price or profitability, which empirical data shows are important factors in expected stock returns. The 500 Index simply weights their holdings by company size, as do many other index funds.

Dimensional Fund Advisors has spent over four decades refining an approach that keeps what works about indexing and active management and throws out what doesn't. Avantis, founded in 2019 by former Dimensional leaders, was built on the same foundation.

Now you may be thinking "okay this sounds plausible, but what are the results?". Over the last 20 years about 78% of Dimensional Funds have outperformed their benchmarks, which is quite different than the 90% failure rate mentioned earlier.

Avantis has a much shorter history with their 2019 inception, but I went ahead and took the 5 original Avantis Equity ETFs that launched and compared their results to their closest Vanguard match. The results are below, and Avantis has won in every category by a good margin despite their slightly higher expense ratios. We first began using Avantis ETFs in 2020 at Meredith Wealth.

.png)

Index funds changed investing for the better, and we wouldn't be where we are today without the work of Jack Bogle and Vanguard. But the investment landscape has evolved. Dimensional and Avantis have built something that honors the core principles of indexing: low costs, broad diversification, discipline, while addressing its structural blind spots. At Meredith Wealth Planning, we don't pick stocks and we don't try to time the market. We build portfolios around what the evidence says about where long-term returns come from. Index funds are a good way to invest. We believe this is a better one.

Disclaimer: Meredith Wealth Planning, LLC is a registered investment adviser with the SEC. This blog post is for educational and informational purposes only and should not be considered investment advice, a recommendation, or an offer to buy or sell any security. All investing involves risk, including the possible loss of principal. Past performance does not guarantee future results. The Avantis vs. Vanguard comparison uses the closest comparable fund for each category; the funds do not track identical strategies or benchmarks. Dimensional fund performance data is sourced from Dimensional Fund Advisors; see the Dimensional vs. Industry graphic for full methodology and disclosures. References to specific securities, funds, or companies are for illustrative purposes only and do not constitute a recommendation. Meredith Wealth Planning and its clients may hold positions in the securities discussed. For more information, please review our Form ADV and Form CRS.

A quick chat to get to know each other and learn more about what you're looking for in an advisor

We know that working with an advisor is a big decision, take some time & sleep on it

When you're ready, we get started with our planning process